BY: Reall

Reliable household income data for emerging markets is often hugely challenging to find, particularly below national or state level.

There are many reasons for this scarcity. Firstly, many households operate within informal economies, where income may be irregular and hard to track. Secondly, there may be reluctance to disclose income, with people having concerns over government surveillance and tax implications. Thirdly, income data is often heavily biased dependant on the data collection method, with respondents potentially underreporting earnings. All these factors effect an emerging market’s ability to produce accurate income data that can inform effective policy making.

This is not only an issue in housing, but across many different industries and sectors. The absence of accurate income data creates significant hurdles for industries like housing, as affordability is a key criterion in meeting demand. To address this gap, Reall has developed a Household Income and Affordability Calculator, which offers much needed insights into income distributions and housing affordability in our priority markets (Kenya, India, Pakistan, Nigeria and Uganda).

Process

With support from Warwick Business School, particularly MSc Business Analytics student Vignesh Parthasarathy, Reall has extracted raw household consumption data (a common proxy for income) from large scale expenditure surveys undertaken by the national statistical offices of India, Kenya, Nigeria and Uganda, plus combined income and expenditure data from the Pakistan statistical office. By sorting the data by monthly household income/consumption and aggregating by sub-national and local regions, we were able to extract percentile figures from the data, giving a picture of household income across locations. Using median annual inflation data since 2010, we can then make broad predictions on current and future income levels.

Raw household data was downloaded from the website of each country’s Statistical office, with simple statistical analysis undertaken by Reall and Warwick Business School. The following surveys were used:

All surveys categorised households based on their county/district and whether this is an urban or rural area, meaning that data can be extracted for individual locations. Unfortunately, outside of the largest cities it is generally not possible to extract data for cities themselves; sometimes counties/districts consist of a single city, but generally they are made up of cities and their surrounding area, or cities comprise of multiple districts.

Additionally, care must be taken when looking at less populous counties/districts, where sample sizes can become too small. As an example, Kampala is the only city in Uganda where more than 100 households were surveyed.

Disclaimer; income and expenditure data is notoriously unreliable, particularly for wealthier groups, as stated in our introduction. This unreliability is multiplied when projecting this data to future years; inflation rates are a poor indicator of changes to income, particularly when those years include the COVID pandemic and the following global cost of living challenges. National inflation rates also mask significant variation across locations and across economic groups. This is discussed in more detail below in relation to Kenya.

This calculator is not attempting to provide definitive figures, but a rough estimation. It will continue to be built on as new surveys are released.

Results

All data below is inflated to 2024 using median annual inflation rates from 2010-23. Median rates were used rather than actual figures to help compensate for large-scale inflation across many economies in 2022 and 2023 (e.g. over 30% inflation in Pakistan in 2023 alone).

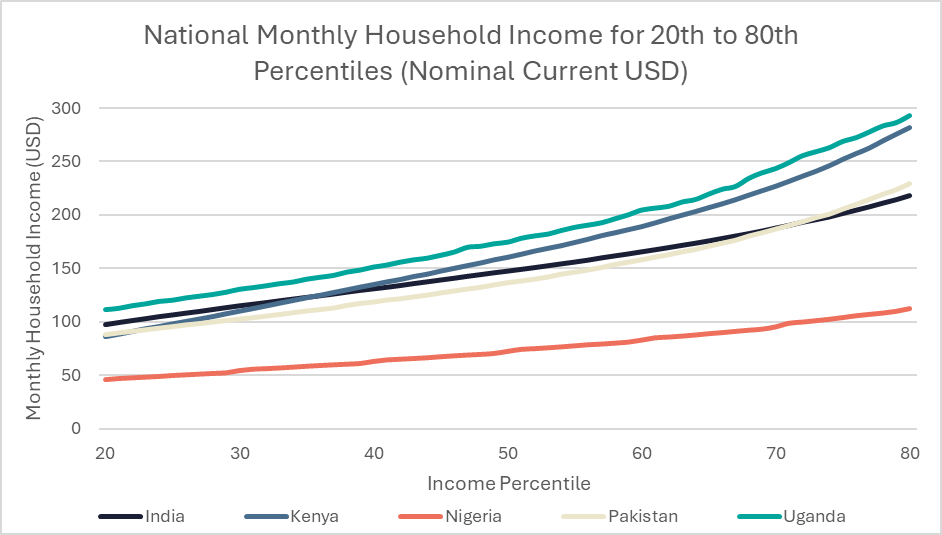

National data is presented below in current USD to enable international comparisons. However, Nigeria shows the problems with presenting data this way; since June 2023, Nigeria’s Naira has dropped from ~NGN 400 = USD 1 to ~NGN 1,600 = USD 1. As a result just eighteen months ago the median household income would be equivalent to ~US292/month rather than the USD73/month it equals now.

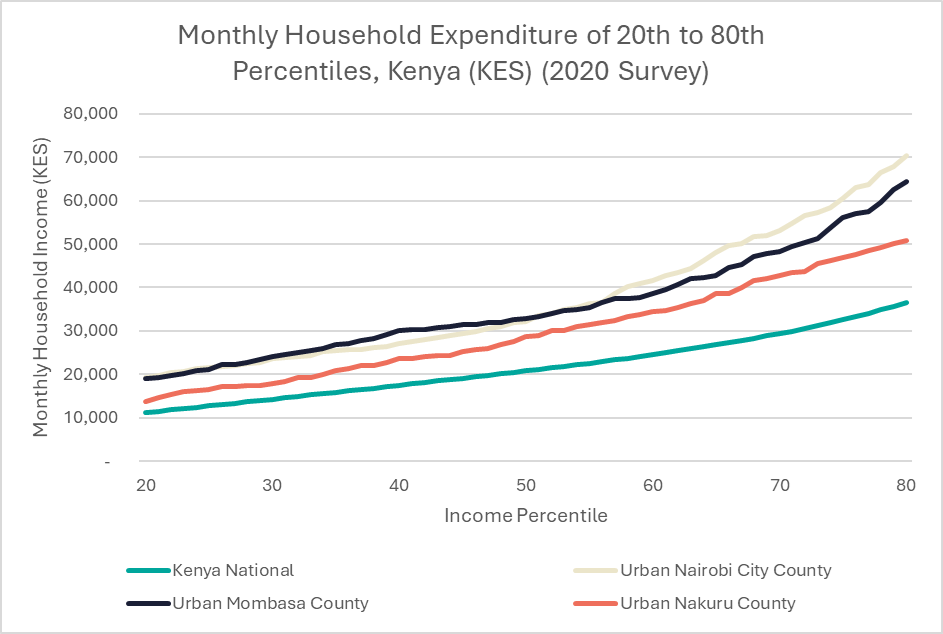

To compensate for rapid growth in incomes at the top of the income pyramid and improve legibility, graphs below show data for 20th to 80th percentiles.

All surveys contain data on number of individuals living in a household, and (other than the Kenya Continuous Household Survey) number of earners within a household. Other than in the case of Pakistan, mean household sizes were generally smaller than might be expected. There is also a significant difference in the mean number of workers between Uganda and Nigeria on one side, and the remaining countries on the other. This may go some way to explaining the slightly higher household incomes in Uganda compared with generally wealthier Kenya.

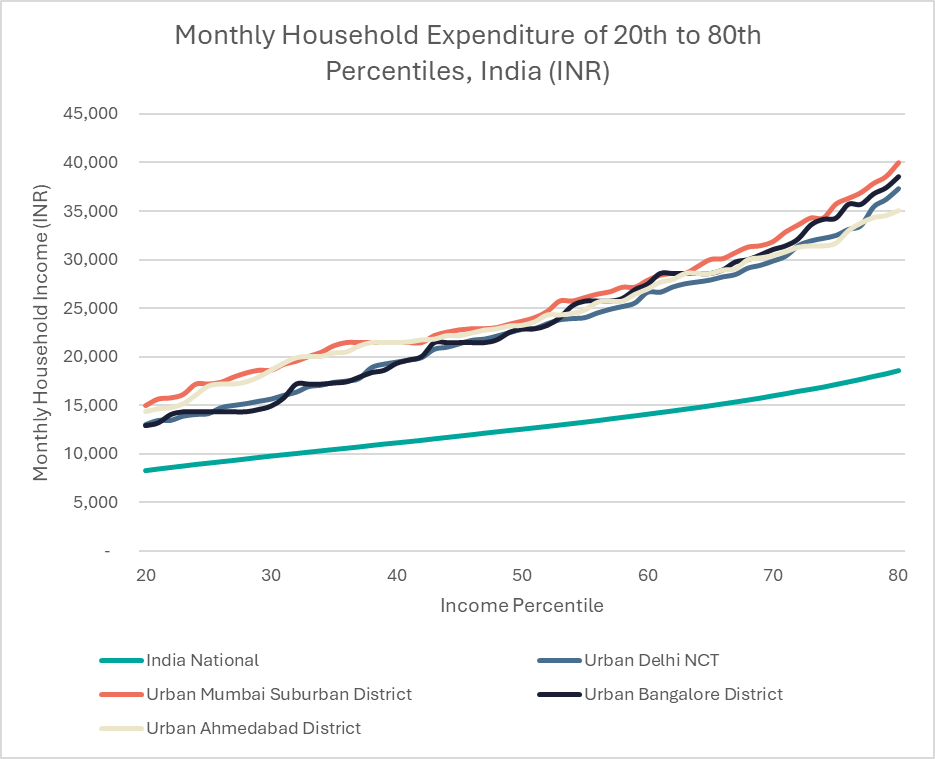

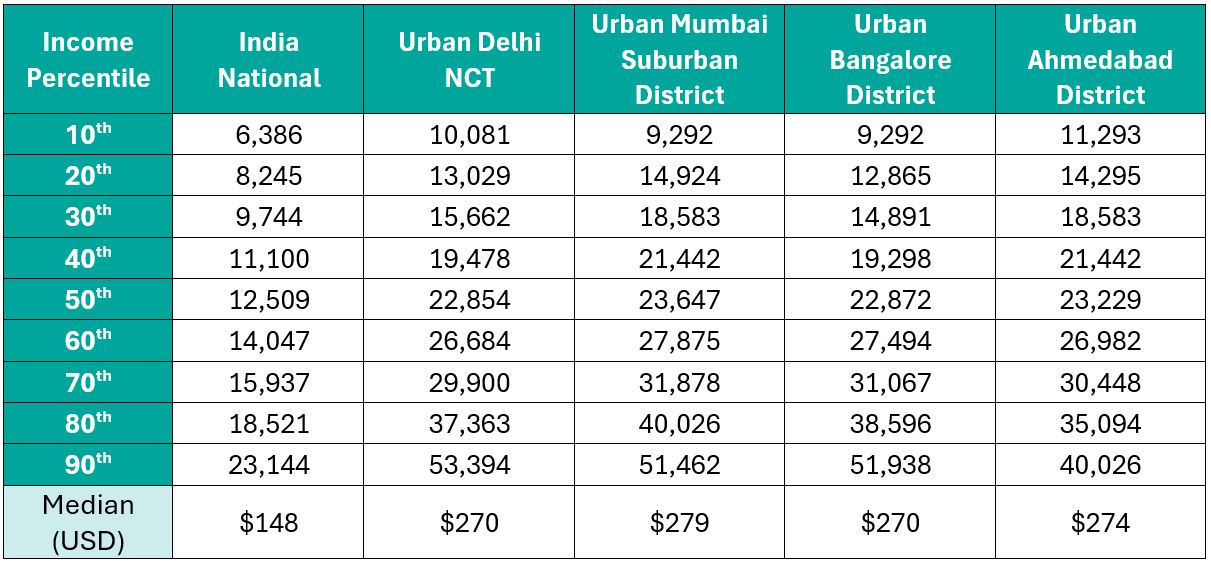

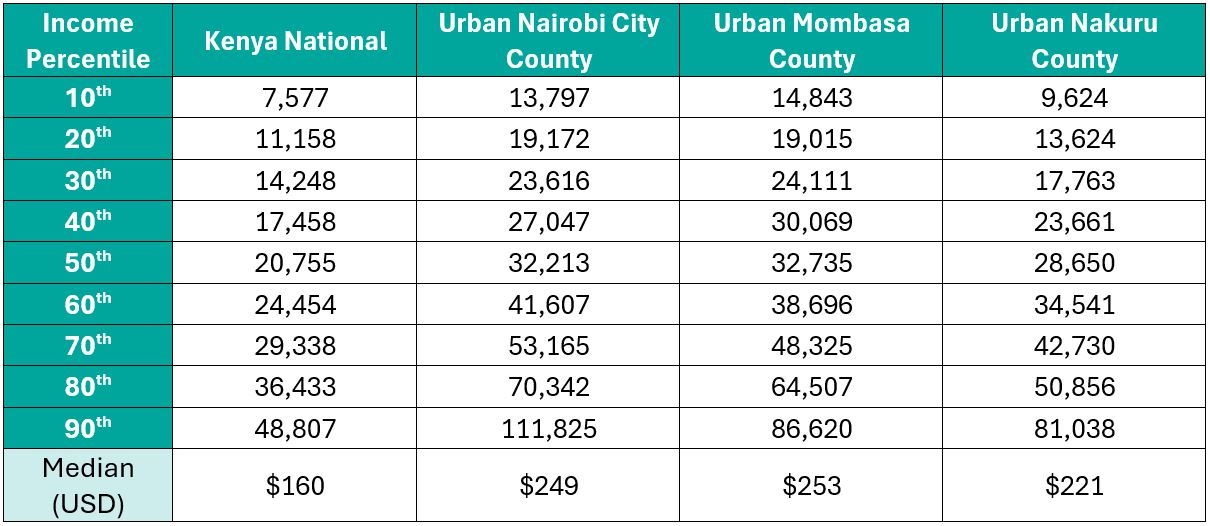

This national level data masks significantly higher incomes and often substantial differences across urban areas, which is demonstrated with Kenya and India below.

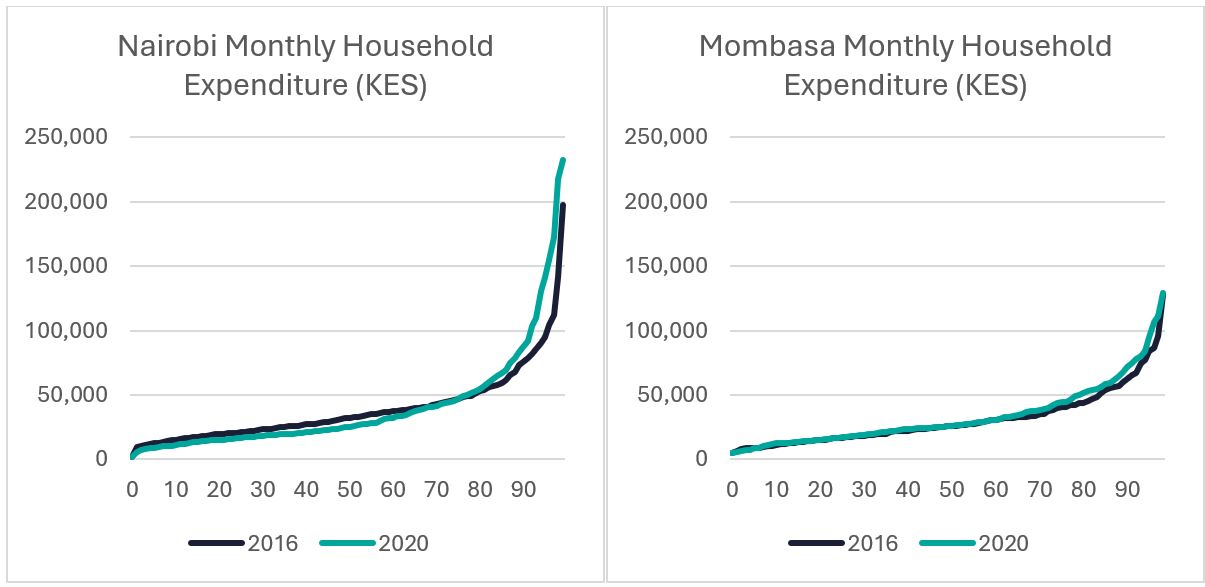

Comparing 2016 and 2020 Kenya Data

As highlighted earlier, the calculator contains data from two different Kenyan household surveys, undertaken by the same organisation using broadly standardised approaches and with similar numbers of households surveyed. This provides an opportunity to test the calculator’s approach to inflation.

We know that inflation is a poor way of measuring changes to household income and expenditure; it measures the changes to costs of goods, but not the quantity that households consume. It also reduces this change down to a single figure that masks what can be substantial differences across locations and income groups.

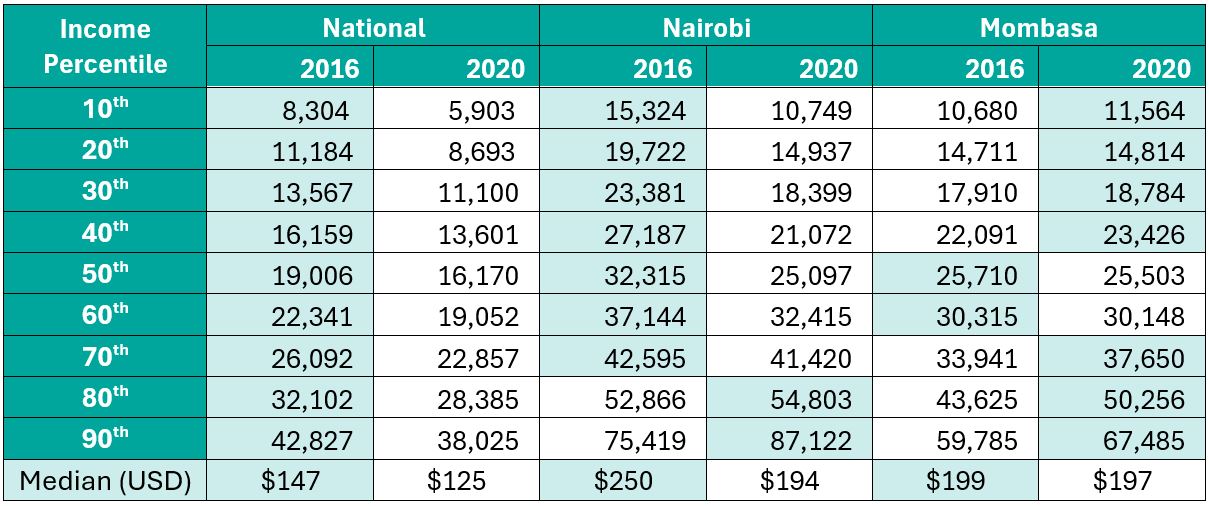

The graphs and table below inflate 2016 data to 2020, and compare this to actual 2020 data. We can see that at a National level, the inflated 2016 figures are quite substantially higher than the 2020 figures (over 40% higher at the 10th percentile, and still 10% higher at the 90th percentile). In fact, for the Bottom 20% of the income pyramid, non-inflated 2016 figures were higher than 2020 figures at a National level, creating a significant decrease in income/expenditure in real terms.

At county level, inflated 2016 figures surpassed 2020 figures in Nairobi for all income groups up to the 75th percentile. Again, this was an over 40% difference at the 10th percentile, though 2020 figures were 15% higher at the 90th percentile. However, in Mombasa, 2020 incomes were higher than inflated 2016 figures for the vast majority of percentile groups. Clearly, further work is required to build a more robust approach to predicting future household incomes.

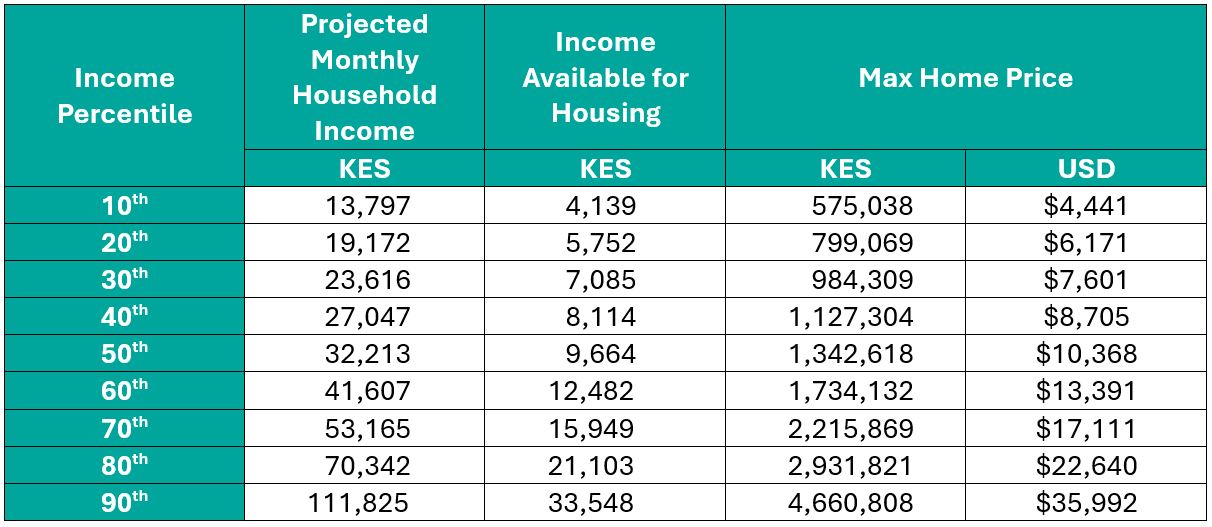

Predicting Maximum Affordable Housing Costs

Using simple adjustable loan terms on proportion of income available for housing, interest rate, down payment and tenor (number of years), the calculator predicts the maximum amount that a household at each income decile can spend on housing per month, and as a result, the maximum affordable home price.

This shows the disconnect between what markets are building and where the demand sits. In Nairobi, Kenya for example, even assuming that 30% of household income can be spent on housing (far above the average amount spent[1]), and subsidised interest rates of 9% over a 20-year period with a 20% downpayment, only 50% of the population can afford a home priced at $10,000 (KES 1.3m). See the Centre for Affordable Housing Finance in Africa’s ‘Housing Developments in the Nairobi Metropolitan Area’ dashboard to explore this gap in more detail.

Conclusion

Reliable household income data is vital in terms of understanding housing markets and targeting interventions. Reall’s Household Income and Affordability Calculator does not pretend to fully fill this gap, but aims to provide realistic estimations and projections that can be used to build market understanding.

Reall’s calculator can be accessed at www.reall.net/calculator, along with papers laying out the methodology used to extract relevant data from each survey. As we seek to incorporate new data and potentially new territories, it will become an increasingly powerful tool for exploring how housing finance can be used to reflect real incomes of families in our emerging markets.

We would love to hear your feedback, criticisms, and ideas for further improvements. Please reach out to ben.atkinson@reall.net.

——————————————————————————

[1] See analysis undertaken by the Centre for Affordable Housing Finance in Africa (CAHF) and 71point4, which using the same 2016 Integrated Household Budget Survey found that renters in Kenya spend an average of 13% of income on housing –